Remittances continue to flow despite global headwinds

Ben Boateng Jr, Tamale, Ghana

December 30, 2023

Ghana is the second largest recipient of remittances in Sub-Saharan Africa (after Nigeria). In two decades, flows through the financial system have increased from US$117.6 million in 2007 to an estimated US$6.4 billion in 2023. According to the World Bank, they contributed 6.2 percent to Ghana's gross domestic product-GDP in 2022 (compared to 6 percent in 2021)1. Data from the International Organization for Migration (IOM-United Nations) show that between 1.7 and 2 million of Ghanaian citizens reside outside of the country in 53 countries (representing around 5.8 percent of the total population). Half of this diaspora are in Sub-Sahara Africa2.

Domestic institutions for remittances

The Bank of Ghana (BoG) supervises operations and transactions connected to remittances. Commercial banks, money transfer operators (MTOs) and mobile phone companies enable and provide remittances services. FinTech companies are making a foray into this segment of the financial services through their respective online digital platforms.

In this institutional setting, the GhIPSS (Ghana Interbank Payments and Settlement System) develops and manages the interoperability of the payment infrastructure with banks, e-money issuers (EMIs), payment service providers (PSPs) acting as enablers. The GhIPSS is a subsidiary of the Bank of Ghana. Interoperability is an important factors in the understanding and calculation of the cost structure of remittances3.

Mobile phone companies (Airtel Tigo Money, MTN Mobile Money, and Vodafone Cash) are critical institutions in the domestic remittance ecosystem. Another major player is the Ghana Post, which pays out remittances through its 700 branches. Over the past decade, Ghana Post has developed its own digital products such as CashPost, e-wallet and debit card. Also, through a partnership with licensed financial institutions, FinTech such as Zeepay, Ghana Post facilitates bill payments.

Customers need the Ghana Card for on-boarding and due diligence in financial transactions. The Ghana card (or Ghana biometric identification card) is the universal proof of identity in the country.

Country channels

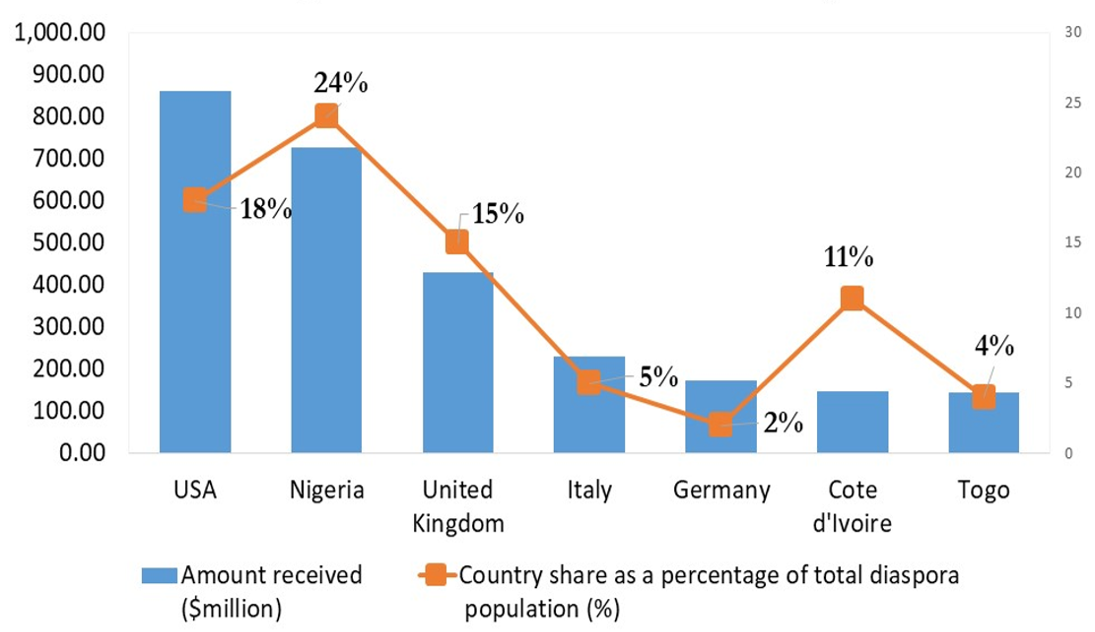

Outside of Africa, the United States follows with 18 percent, the United Kingdom (15 percent) and Côte d’Ivoire (11 percent). Fifteen percent of the Ghanaian diaspora live in Europe, where the UK hosts the largest community, followed by Italy (51,364) and Germany (27,872)4. Global data show that 49 percent of Ghanaian migrants live in sub-Saharan Africa, with 20 percent of migrants living in neighboring countries. Côte d’Ivoire leads with 111,024, Togo (47,093) and Burkina Faso (33,225). Also, on the African continent, Nigeria has the largest Ghanaian diaspora with 24 percent of the population.

Share of remittances inflows vs size of diapora 2020

Data compilation: www.neweconomyghana.com

The presence of a large diaspora population in rich countries does not necessarily translate into substantial remittances. Together, the diapora in neighboring countries such as Côte and Togo, remit more money back to Ghana, than those who live in certain rich countries (in Europe and North America). Remittance data presented here, from Ghana's neighbors do not include informal cross-border remittances (from Côte, Burkina Faso and Togo) to Ghana.

Economic impact and risks

At the microeconomic level, remittances provide financial help to millions of households in Ghana. They also have a significant impact at the macroeconomic level. In 2023 for example, after a year of economic turbulence, the balance of payments improved thanks to higher remittance inflows and decreased outflows from the debt standstill5. Ghana also provides evidence that remittances tend to have counter-cyclical characteristics at the macro level. This means that ‟remittance flows tend to be more stable than capital flows, and they also tend to be countercyclical—increasing during economic downturns or after a natural disaster in the migrants’ home countries, when private capital flows tend to decrease”6. However, the economic realities of each country can distort or correct these inferences. This is because the growth of remittances partly depends on the size of the diaspora population, their earning power, and the strength of the economy of the country where they live.

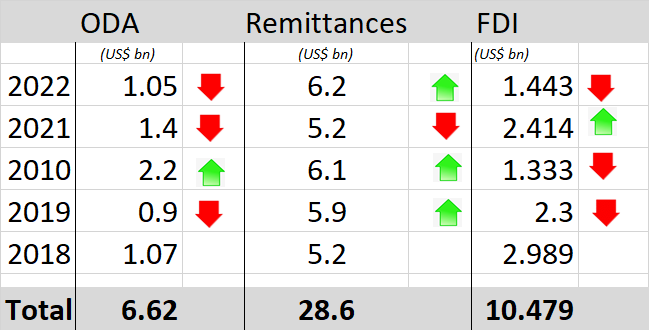

Policy makers agree that remittances inject cash into the economy of Ghana and that the inflows exceed foreign direct investment and foreign aid.

Growth of remittances vs ODA and FDI

Sources: One.org, UNCTAD, World Bank7

A powerful source of volatility in remittances is tied to the economic conditions of the host countries. COVID-19 demonstrated a positive correlation between deteriorating economic conditions outside of Ghana and low remittances inflow. When economic conditions deteriorate, a fall in remittance ensues. However, remittances flowing from Nigeria to Ghana remained constant during the pandemic. This suggests that Nigeria ought to be a target country for future policy design for optimal benefits from remittances.

Another risks stem from the continued tightening of immigration policies around the world. A reduction of Ghanaian abroad may results in lower inflow of remittances. According to IFAD, the pace of international migration has declined for Ghana by 12 percent since 2015. Tougher migration conditions in host countries explain this decline. A domestic policy like the ‟Year of Return” also harbors potential unexpected and undesired adverse effects. Specifically, more Ghanaians returning to live in Ghana may mean fewer remittances.

Related Articles

BIBLIOGRAPHY

1❩ Remiscope Africa (2023): Ghana Country diagnostic - https://remitscope.org/wp-content/uploads/2023/06/Diagnostics_Ghana_2023_preliminary_release.pdf

2❩ Remiscope ibid.

3❩ The State of Instant and Inclusive Payment Systems (SIIPS) in Africa 2022 https://ghipss.net/index.php/publications/downloads?download=16:the-state-of-instant-and-inclusive-payment-systems-in-africa-siips-2022-case-study

4❩ Ministry of Foreign Affairs and Regional Integration (2019): Diaspora engagement intiative - https://ghanaemberlin.de/wp-content/uploads/2019/12/DAB_CONCEPT_PAPER.pdf

5❩ World Bank (2024): Preserving the future: rising to the youth employment challenge (8th Ghana Economic Update June 2024) - https://www.worldbank.org/en/news/press-release/2024/07/22/ghana-economic-prospects-on-track-amid-reforms

6❩ https://www.imf.org/en/Publications/WP/Issues/2023/05/05/Remittances-and-Social-Safety-Nets-During-COVID-19-Evidence-From-Georgia-and-the-Kyrgyz-532625

see also

Dilip Ratha (2009): Remittances: Funds for the folks back home in Finance and Development (IMF) https://www.imf.org/en/Publications/fandd/issues/Series/Back-to-Basics/Remittances

7❩

World Bank (2023): Ghana net ODA - https://data.worldbank.org/indicator/DT.ODA.ODAT.CD?locations=GH

see also

World Bank (2023): Personal remittances - https://data.worldbank.org/indicator/BX.TRF.PWKR.CD.DT?end=2023&start=2023&view=bar